Smartworks Q3 results

The Indian coworking and managed office operator space has silently emerged as one of the strongest structural growth opportunities in commercial real estate. What was once driven largely by startups and freelancers is today being powered by Global Capability Centers (GCCs), large MNCs, and scaling Indian enterprises who need plug-and-play office capacity without the friction of owning or managing real estate.

Walk into any major Indian city – Mumbai, Pune, Bengaluru, Chennai, Gurgaon – and you see the same pattern: Grade-A commercial buildings with names of coworking operators mounted on their facades. Among these, Smartworks stands out as the largest and most dominant player by seat capacity and institutional clientele.

This quarter’s numbers reinforce a key underlying trend: demand is not just strong; it is formalizing and premiumizing.

Why the Coworking Operator Model Is in a Strong Cycle

Three secular forces are driving this theme:

1. GCC Expansion in India

Global Fortune 500 and Fortune 2000 companies are increasingly using India for:

- back-office functions

- tech development

- shared services

- design and analytics

- compliance and operations

These companies don’t want to build or buy office buildings. They want solutions. Their ask is straightforward:

“Give us 500/1,000/2,000 seats in this location with cafeteria, meeting rooms, security, IT infra, parking, and amenity stack.”

Coworking operators solve precisely this.

2. MSME & Startup Scaling

Indian companies like Urban Company, Lenskart, and numerous SaaS/Tech startups scaled massively in the last decade. Scaling requires:

- more employees

- better retention environment

- well-designed offices

Employees no longer want to work in dim, cramped, low-quality spaces. Workspace aesthetics directly influence employer branding, productivity, and culture.

3. Premiumization of Commercial Real Estate

There is a clear shift toward Grade-A assets offering:

- better ventilation

- ESG & sustainability compliance

- parking & transit access

- gyms, creches, cafeterias

- safer late-night commute

These amenities matter especially for MNCs, GCCs, and high-utilization offices.

Smartworks Business Model in Brief

Smartworks follows a clean and very scalable model:

➤ Step 1: Long-Term Take on Lease

Smartworks leases bare-shell buildings from landlords like DLF, Hiranandani, etc. under 10–15 year straight leases (not revenue share).

➤ Step 2: Converts to Premium Office Campus

Smartworks invests in fit-outs:

- electrical

- mechanical

- plumbing

- furniture

- workstations

- meeting infrastructure

and rebrands the building under the Smartworks identity.

➤ Step 3: Sub-Leases to Institutional Clients

Clients include:

- MNCs

- GCCs

- IT/Tech

- BFSI firms

- Unicorns & growth startups

This generates a net rental spread between lease rent paid vs. sublease rent earned.

Since lease rent is largely fixed, higher occupancy directly expands margins via operating leverage.

Smartworks’ Strategic Positioning: Focus on Large Clients

Unlike smaller coworking operators who sell desks to freelancers or very small teams, Smartworks targets:

- multi-city clients

- multi-year contracts

- 1,000+ seat deployments

Over 40% of revenue is estimated to come from such clients, de-risking occupancy and boosting utilization consistency.

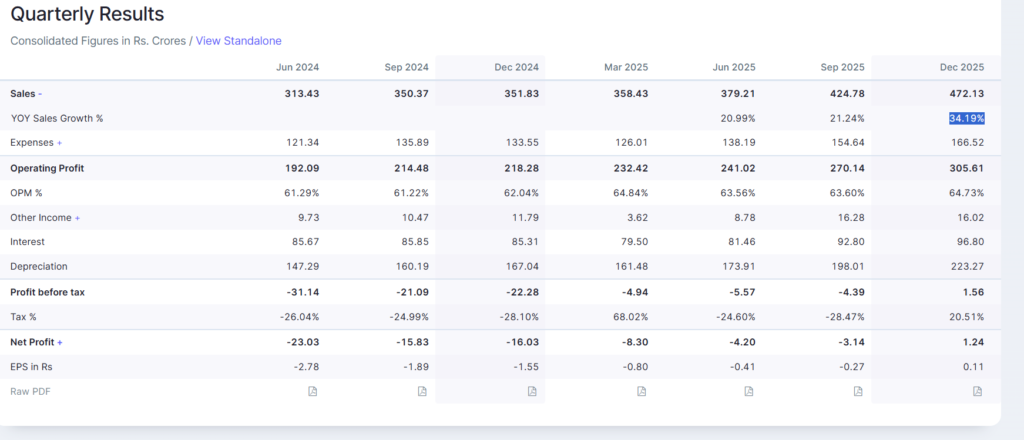

Q3 Results:

The numbers this quarter validate the business flywheel:

✔ Revenue Growth Accelerates

- Earlier growth post-IPO: ~20% YoY

- Q3 YoY growth: 34%

A clear step-up in execution and absorption.

✔ First Quarter of Profitability

Smartworks reported profit for the first time. The profit pool is still small (~₹1–2 crore), but the direction matters more than the magnitude.

The journey is visible: loss → smaller losses → breakeven → profitability

✔ Operating Leverage Expands

Operating metrics also improved:

- EBITDA margin: from ~16% → 18%+

- ROCE: from ~13–14% → 21%

This is classic real-estate utilization leverage: older buildings turn profitable as they mature.

✔ Occupancy Above 90%

Occupancy remains extremely healthy, supporting further margin expansion.

✔ Visibility of Supply

Management highlighted that supply is locked for:

- FY26

- FY27

capex work is ongoing.

This eliminates a major bottleneck for scaling.

Why Operating Leverage Matters Here

Once a building crosses utilization threshold and hits breakeven, incremental seats contribute disproportionately to profitability because:

- rent = fixed

- utilities = largely fixed

- manpower = largely fixed

- incremental seating = high-margin revenue

Thus, as seat absorption rises, ROCE expands sharply.

This is exactly what Smartworks is now demonstrating.

Sector Implications

Smartworks, as the leader, becomes the benchmark. Smaller listed peers like:

- IndiQube

- AWFIS

- Contour

- EFC

will now be judged relative to Smartworks’ pace. At a lower base, if they grow slower than Smartworks, it raises questions on competitive positioning.