Solar Story over ? Let’s Decode

For a few years, solar energy was treated like a once-in-a-generation theme in the Indian market.

Government push, PLI schemes, net-zero targets, rooftop subsidies – everything was in favour of the narrative.

Stocks rallied hard. Then reality showed up.

In the last 1–2 years, many solar-related names – especially module manufacturers, EPC players, and ancillaries – have seen sharp corrections from their highs. The sector still has a strong long-term story, but near-term, the pain is real.

So what went wrong? Is it just oversupply, or something deeper?

Let’s break down the Indian solar crash in a structured way, with company-level context.

1. Big Picture: India’s Solar Boom Turned into a Mini-Capex Cycle

India aggressively pushed domestic solar manufacturing:

- Multiple companies announced multi-GW module and cell capacities.

- Policy support via BCD, ALMM, PLI led many entrepreneurs to jump in.

- At the same time, global capacity – especially from China – exploded.

According to Wood Mackenzie, India’s solar module manufacturing capacity is on track to exceed 125 GW by 2025, while domestic demand is around 40 GW – that’s more than 3x local requirement, implying a sizeable inventory build-up if exports don’t absorb the surplus. (Wood Mackenzie)

An SBI-linked analysis highlighted that India started exporting large volumes of modules (5.8 GW in 2024, 3x the previous year), mostly to the US, but rising US tariffs are now threatening that export route. (Solar Magazine)

Net result:

We created a manufacturing boom faster than demand – classic capex cycle + oversupply setup.

2. How Oversupply Hits the P&L

Oversupply doesn’t just mean “zyada factories bane hai”. It directly hits the financials:

- Module ASPs crash

- Global module prices fell sharply as Chinese players prioritized volume over margins.

- Domestic companies face price wars, lower realizations, and thinner margins.

- Inventory losses

- Stocks bought at higher prices lose value as prices fall.

- This hurts gross margins and may show up as inventory write-downs.

- Working capital stress

- Customers delay purchases expecting even lower prices.

- Payment cycles stretch, receivables go up, debt increases to fund this gap.

- Valuation de-rating

- Markets earlier valued solar names on “mega-theme” narratives.

- Once earnings don’t match the hype, multiples compress sharply.

Too much of future optimism was earlier factored in which is now getting de-factored as the valuations get compressed.

3. Segment-Wise: Who Is Getting Hit?

The impact isn’t uniform. Let’s look at key segments in the Indian solar chain.

(a) Module & Cell Manufacturers

These are most directly exposed to oversupply and price wars.

- Huge capex cycles.

- High fixed costs.

- Heavy dependence on policy protection and export markets.

- ASP and margin volatility.

Case: Insolation Energy (INA Solar)

Insolation is a fast-growing Indian module manufacturer. For FY24–25, it reported ~81% revenue growth to about ₹1,333–1,334 crore and net profit growth of ~127%, with strong EBITDA expansion as well.

Future plans include scaling up to 8 GW module capacity, 3 GW cell capacity, and a large aluminium frame capacity by FY25–27 – clearly betting on continued demand and domestic self-reliance.

But here is the catch from an investor’s perspective:

- The sector is in oversupply.

- Exports to the US face tariff risk.

- If module prices fall faster than costs, margins can compress sharply.

- Inventory and receivables need careful monitoring.

So even though the reported numbers look strong, the market worries about cycle risk, oversupply, and whether such aggressive capacity will earn sustainable returns. That’s why you often see sharp stock price volatility despite good headline results.

(b) IPPs + CPP / C&I Focused Players

These companies are more like project developers + power producers, not pure manufacturers.

Case: KPI Green Energy

KPI Green works with a dual model:

- IPP (Independent Power Producer) – owning solar assets and selling power.

- CPP / Captive / C&I EPC – setting up solar plants for industrial/commercial customers.

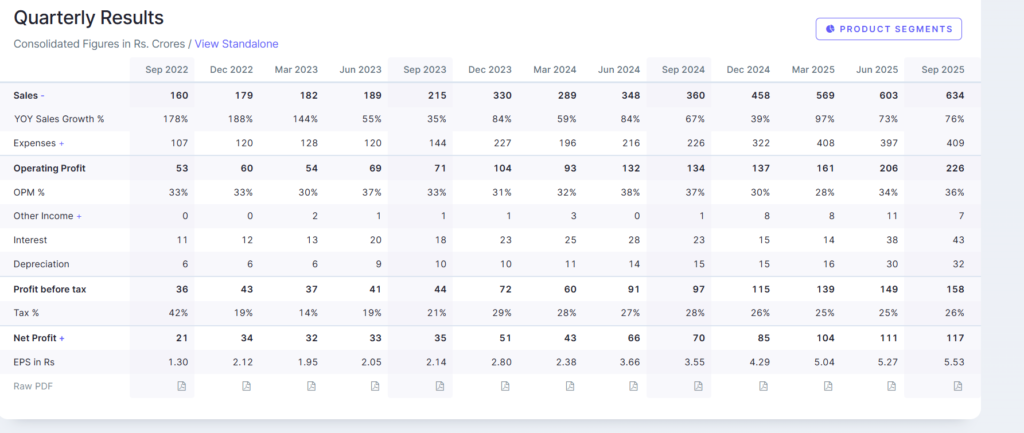

Over FY15–FY24, KPI’s revenue has grown strongly, with operating profit margin in a healthy 30%-plus range in recent years. For the 12 months ended Sept 2024, KPI reported NPM around 17% and OPM near 33% – clearly a profitable, high-ROE profile during good times.

The company reported a strong 76% YoY growth in sales in Q2FY26, reflecting continued business momentum. The stock had delivered stellar returns earlier driven largely by P/E re-rating, but post that phase it has entered a healthy consolidation zone with a sideways trend.

But risks for such players are different:

- Execution risk: delays in land, grid connectivity, and regulatory clearances directly hit revenue.

- Receivable risk: dependence on counterparties – DISCOMs, industrial customers – for timely payments.

- Interest rate & leverage: IPP business is debt-heavy; higher interest costs hurt equity returns.

- Tariff pressure: intense competition and aggressive bidding can compress project IRRs.

Stock crashes here are less about module oversupply and more about:

- stretched valuations after a big run-up,

- concerns around receivables/leverage,

- and whether growth rates are sustainable.

(c) Ancillaries: Solar Glass, Structures, BOS (Borosil Renewables)

Ancillary players sell inputs into the solar ecosystem – glass, structures, cables, etc.

Case: Borosil Renewables

Borosil is India’s leading solar glass manufacturer.

It invested heavily, including acquiring a large solar glass business in Europe. But global solar glass went through a period of overcapacity and price pressure, especially due to cheap Chinese and Vietnamese imports.

- The company has now decided to wind up its German unit and refocus on India, after weak European economics and dumping pressures.

- In India, Borosil is once again expanding capacity. It plans to go from about 1,000 TPD to 1,500 TPD solar glass capacity, backed by a ~₹900–950 crore capex.

- A recent “reference price” notification for imported solar glass is meant to protect domestic producers from ultra-cheap imports. (Indian Chemical News)

Market fear here is simple:

- Solar glass is highly cyclical.

- Capex is large, returns can be volatile.

- Global oversupply can again crush margins if protection is diluted.

So even with supportive policies, stock prices can swing sharply as investors keep reassessing cycle vs. structural.

(d) Large Integrated & Utility Players (Adani Green, Tata Power, etc.)

Bigger players – like Adani Green, Tata Power Renewable, JSW Energy (renewables pivot) – sit in a slightly different bucket:

- They benefit from scale, cheaper funding, and integrated portfolios.

- But they still face:

- regulatory risk,

- execution challenges,

- tariff caps,

- and global sentiment on “green valuations”.

Global sentiment has turned more cautious on green energy overall – for example, even BP recently took a multi-billion-dollar write-down on its renewables/transition assets, admitting that earlier assumptions on the pace of energy transition were too optimistic.

When the global market de-rates renewables as an asset class, Indian names also feel the heat.

4. Why Are Solar Stocks Crashing Now?

Let’s put it all together. The current correction in Indian solar stocks is driven by a mix of:

- Oversupply & Capex Hangover

- Module capacity far above near-term domestic demand. (Wood Mackenzie)

- Export dependence facing policy barriers (like higher US tariffs). (Solar Magazine)

- Narrative vs Numbers Gap

- Managements across the space gave rosy guidance – big capex, huge revenue targets, ambitious margin commentary.

- When actual quarterly numbers show:

- margin pressure,

- stretched working capital,

- or slower execution,

valuations de-rate sharply.

- Retail FOMO Unwind in SME/Small Caps

- Many solar plays listed on SME or midcap platforms saw euphoric rallies.

- Once sector headwinds became visible, these became prime candidates for profit booking and exit liquidity.

- Global Risk-Off on Renewables

- Higher interest rates globally reduce the attractiveness of long-gestation green projects.

- Large global players resetting expectations drags down sentiment for the entire theme.

- Policy Whiplash

- ALMM pause and re-imposition, varying duty structures, changing export routes…

- All this increases uncertainty and discount rate in investor models.

5. Is the Solar Story Over in India?

The story isn’t over – it’s only reset. Now is when serious investors start tracking the sector closely, because that’s how real opportunities quietly emerge.

Structurally:

- India has huge energy demand growth.

- Net-zero and renewable targets are not going away.

- Rooftop, C&I, and hybrid projects (solar + wind + storage) have a long runway.

- Government is still pushing domestic manufacturing and PLI.

But the path will be:

- more cyclical,

- more competitive,

- and less “straight line” than the early narrative suggested.

The market is transitioning from:

“Anything solar will do well” → “Only disciplined, competitive solar businesses will create value.”

6. What Should Investors Track Going Forward?

If you’re tracking or holding solar names, some key check-points:

- Utilisation vs Capacity

- Are plants running at healthy utilisation, or is capacity lying idle?

- ASPs & Margin Trend

- Are ASPs stabilising?

- Is gross margin improving, or still under pressure?

- Working Capital Discipline

- Receivable days.

- Inventory days.

- Short-term borrowing trends.

- Leverage & Interest Coverage

- Especially for IPP and capex-heavy players.

- Policy & Trade Actions

- Anti-dumping duties, reference prices, ALMM status, US/EU import policies.

- These can swing economics overnight.

- Quality of Growth vs Just Quantum of Growth

- Profitable, cash-generating growth is different from debt-fuelled capex + thin-margin volume.

7. Closing Thoughts

Indian solar stocks are not crashing because the energy transition is dead.

They are correcting because:

- the market front-loaded too much optimism,

- the supply side ran ahead of demand, and

- now we are living through the hangover phase of a capex cycle.

From here, returns will likely be made not by buying any solar name, but by picking:

- companies with cost advantage,

- clean balance sheets,

- rational capex plans,

- and managements that under-promise and over-deliver, not the other way around.

DISCLAIMER : This post is purely for educational purposes and all the stocks discussed here are for case studies. This should NOT be taken as a recommendation in any form.