Company showing a clear shift from being just a pipe manufacturer to becoming a broader infra steel products company. The company has introduced crash barriers, transmission line towers and poles, with monopoles planned next. These segments carry higher margins than traditional pipes, which can gradually lift profitability as the mix improves.

The Odisha plant is turning into the key growth driver. Its location gives raw material and logistics advantages, and it opens up new markets in the East, Northeast and exports.

Dispatch ramp has been faster than expected, and demand has come both from pipes and crash barriers. This plant essentially fills a geography gap that Vibhor could not address earlier.

The broader environment has also turned positive – steel prices are up, anti-dumping measures against China are in place and infra activity remains strong. Management indicated better order flow, healthier pricing and improving execution in H2.

Working capital remains comfortable and there are no signs of stress in the system. So near about 20% sales growth they have shown on YoY basis so further value escalation should give them necessary boost.

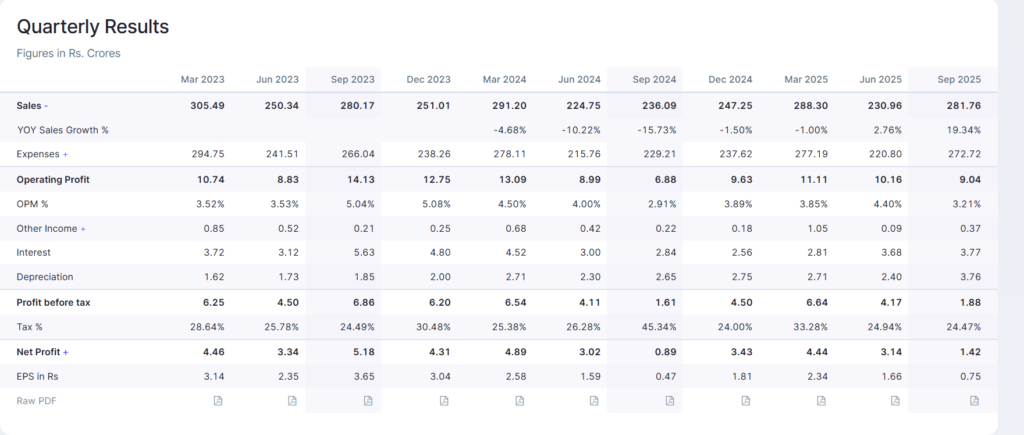

Its sales momentum is gradually returning, with the company delivering 20% YoY growth in Q2. However, for operating leverage to truly play out, we need value growth alongside pure volume growth.

As of now, that leg hasn’t picked up meaningfully, so the overall engine isn’t firing at full strength yet.

Overall not a good bet when I have better companies to invest in or track. Not a recommendation.

DISCLAIMER : This post is purely for educational purposes and is NOT a recommendation in any form. We are only discussing educational insights and this by no way is any recommendation to buy or sell. Please consult your financial advisor.

Loved this blog!

How much can a lift in anti-dumping duties may affect Vibhor negatively?

Yeah government will do everything to protect the industry but again they need to continue to innovate with their product mix to remain competitive in times to come.

At the last it’s commodity,need to know how to play Commodity cycle .

Can’t sustain EBITDA and PAT

With price escalation in steel prices, value growth can come back so that is what we would have to track alongside volume growth.